Unpacking confusion, contention, concern and conflicting narratives on data center and water risks

Written by Josh Weinberg, Senior Policy Advisor, AGWA and Georgette Mrakadeh-Keane, Communications Lead, AGWA

Advancement of computing and artificial intelligence is having transformative impacts on how people live, work and interact across societies. We are witnessing a rapid acceleration of technological solutions and scientific discovery as a result. It is also bringing forth the rise of a new industry and infrastructure for data centers.

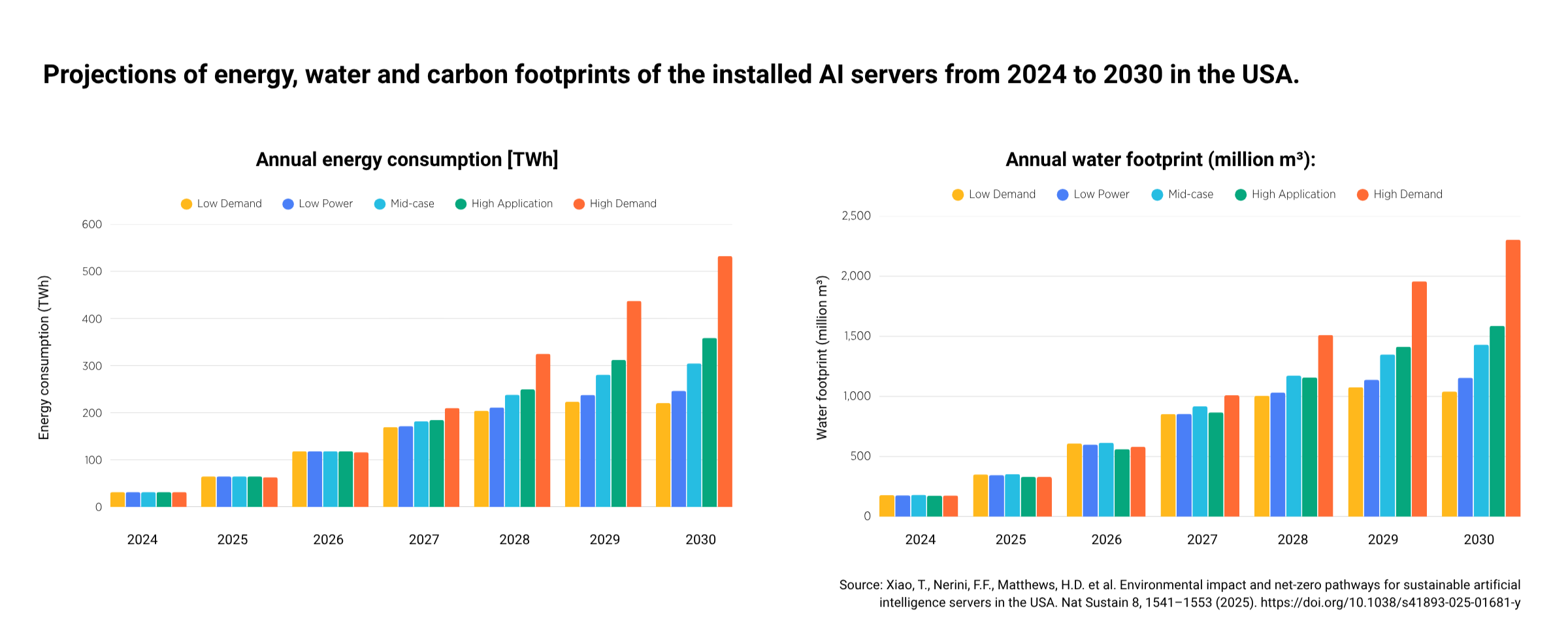

Global capital expenditure to build, upgrade and operate data centers — covering the construction, land costs, cooling and power generation — is projected to reach 2-3 trillion USD over the next five years. The investment in the chips and hardware inside the data centers is even greater, with projections reaching 4 trillion USD over the same period. The pace of growth can present a challenge where development timelines are outrunning the systems designed to manage them. One of the fastest growing regions for the development of this infrastructure is found in Asia-Pacific, where experts have estimated that between 800 billion and 1 trillion USD will be invested to build digital infrastructure in the next few years (with about half of this taking place in China and Taiwan).

Data centers require land, materials and electricity to operate. They can also require water directly for cooling and indirectly in the generation of the electricity they use — particularly if it depends on thermoelectric power plants commonly used for nuclear, coal, natural gas or for hydropower. The key challenge is to ensure that the infrastructure built today is optimized to ensure that its water and energy use do not create increased risks for shortages, higher costs of services or environmental harm in the regions where they are built.

Water resilience is a crucial part of the equation for the sustainable development of digital infrastructure. Any operation dependent on water for cooling will face major operational risk if access to the required water is lost at any period of time. Even if direct access to water for cooling is maintained, negative impacts to local water sources and services for residents that emerge in areas with data centers can create reputational risks, loss of social license to operate and impede future opportunities.

In the Asia-Pacific region, most of the areas with the greatest development of data centers — from Jakarta in Indonesia to Johor in Malaysia or Delhi, Chennai and Bengaluru in India — are located near large population centers where water resources are scarce and under pressure. Those same regions also feature energy grids that are currently dominated by coal and natural gas, with relatively large water demands. Malaysia’s rapid growth in the data center market in Southeast Asia has been forced to respond to water impacts by creating stronger regulations and incentives to reduce water use. In drought-prone tech hubs like Chennai and Bengaluru, operators are facing severe delays in securing "Consent to Establish" permits from local pollution control boards, as civic groups increasingly highlight the conflict between massive hyperscale water footprints and the rolling municipal water shortages faced by residents.

Understanding the Players and Pressures

Coordination and action across different stakeholder groups is crucial, including the hyperscalers and data center developers, national and local governments, utilities, investors and community groups. Each faces distinct challenges and potential opportunities to ensure benefits of data center development outweigh risks.

National Authorities

Understanding the challenge and opportunity

National and local governments can be under pressure to attract part of the new trillion dollar digital infrastructure economy, while also seeking to build out their own national infrastructure to host critical data within their borders. The first wave of data center growth has seen heavy consolidation within regions which have been able to provide known solutions for land, energy and connection to grids.

What they can do

Governments can leverage their purchasing power and national markets to regulate efficiency. National governments can also be important customers for data center services and utilize their procurement processes to ensure compliance with water and energy efficiency standards. In Australia, for example, achieving thresholds for the NABERS (National Australian Built Environment Rating System) ratings are becoming mandatory to gain government contracts, and failure to maintain those ratings could lead to a loss of the procurement.

They can also mandate water management plans and impose requirements for planned actions to reduce water demand, utilize alternative water sources and prevent environmental impacts before a data center receives approval for construction.

Some countries have created data localization laws (such as India and Indonesia), which requires that financial and critical government data are stored within their borders. Hyperscalers will invest to build data systems locally to have access to their markets, which means that they can demand environmental performance for that access. In addition, regulators can require or heavily incentivize the use of efficient technologies (like direct-to-chip liquid cooling or closed-loop systems) in larger centers.

Water Utilities

Understanding the challenge and opportunity

The arrival of large new industrial customers brings both challenges and an opportunity to water utilities. Water utilities need to plan for potential water demands from data centers and license accordingly, but this can be a challenge as the pace of data center development — with new facilities constructed within 1-3 years — moves faster than traditional water infrastructure planning. They must respond quickly to assess impacts on water supply, wastewater treatment and their services provision to residents and other users.

What they can do

First, local water utilities should be involved from early stages of the approval and planning process before data center projects are approved. They also should prepare to understand the options, obligations and capacity to meet regional data center development demand. Utilities can ensure their water allocations and pricing incentivize the use of recycled water. If there are existing recycled water production sites or new facilities to be built, they can encourage siting data centers in areas nearby. They can also negotiate, through infrastructure agreements or water service agreements connection and use fees, cost sharing, and asset ownership and operational responsibilities. Water utilities can connect with the growing communities of practice and guidance being developed in a number of countries and regions where data center growth has been greater to expand their capacity and knowledge of how to manage the fast-evolving industry’s impact on their operations.

Investors & Financing Agencies

Understanding the challenge and opportunity

Data centers and digital infrastructure are an attractive asset class with high forecasted growth and steady return on investment. Institutional investors — such as private equity firms, sovereign wealth funds and massive pension funds — are primary sources of billions of dollars of capital investment in the Asia-Pacific region. Institutional investors must mitigate risks to investments, with high level concerns over scenarios where operations halt due to shortage of water or conflicts with local communities and governments. With growing scrutiny of ESG risk performance and public perception of social and environmental risks posed by data center developments on the rise, investors are looking to insulate from reputational risks as well. There is also opportunity to reach wider groups of investment capital by complying with criteria for green and sustainability linked loans and bonds.

What they can do

Institutional investors, particularly those offering specialized sustainability loans, can compel upfront investments from data center builders in improved technologies to install closed-loop or liquid cooling systems through creating this as criteria for “green premiums” or favorable loans. This group can facilitate longer-term investment perspectives that provide both environmental benefit and cost saving over time while requiring larger upfront capital expenditures. As another lever for impacting data centers, they can mandate reaching efficiency targets and other metrics. Active investors can also force increased clarity in the reporting of water consumption and impacts.

Local Communities

Understanding the challenge and opportunity

Data centers are essential, profitable infrastructure for the modern world. But they do not directly provide services to a local area. For local communities, the primary drivers to support proposals to develop data centers are economic. Investments are expected to lead to job creation and tax revenues to the local government and payments to utilities for land, energy and water use. While initial infrastructure construction brings jobs, once built they primarily contribute as a consumer and customer — by paying for energy, water and land resources used to public authorities or private vendors and by paying taxes. There are increasing reported cases of local populations expressing concern that their rates and access to energy and water may increase, or be disrupted, at times of peak demand from data centers. For all parties involved — from the investors, to the data center industry to the government authorities that approve data center projects – minimizing these risks is critical.

What they can do

Local stakeholders can engage with municipal governments to promote actions to create community benefit assessments and agreements that are paired into the approval process for construction and continued operations. They can engage with the mandate of providing the social license to operate and define targeted benefits and conditions that can be stipulated in contracts and community benefit agreements. Depending on the specific local conditions and agreements, there are a number of potential items that may be possible to negotiate. Water-specific items that can be included in data center agreements and licensing range from setting daily water usage caps, monitoring and measurement on water quality impacts, mandates for usage of non-potable water sources and clauses to require capex investments be made by data center customers for additional water infrastructure required to meet additional demands.

Hyperscalers & Data Center Developers

Understanding the challenge and opportunity

Data center developers operate in a fast-paced, competitive environment. Achieving speed-to-market is imperative — and their own operational resilience requires first securing access and rights to water and energy. A standard progression will see first consideration to managing their direct water risk by ensuring required access to water for cooling, and minimizing any risks around water-based disruptions to energy supplies. As wet-cooling is generally more secure and cheaper, operators may need to be incentivized, compelled and aware of risks to compel investment in advanced technologies or use of alternative water sources, like recycled water. For the larger data center actors, water resilience has direct impacts in the supply chain — particularly of the semi-conductors in the hardware of the data center.

What they can do

Hyperscalers can engage in water resilience planning on three levels. Beginning in the planning and siting phase, they can plan for the water resilience for data centers by assessing the required access to water for cooling, minimizing any risks to water-based disruptions to energy supplies to data centers, and focusing on onsite measures and actions to minimize water consumption and impacts in data centers operations. They can also expand engagement and strategic investment across a water and energy-shed to ensure uninterrupted services and affordable costs to residents, and the ecological health of the natural ecosystem. High-tech industries can also be well positioned to provide investments to support water efficiency or improve environmental health in other ways across a watershed. This includes supporting applications of AI to improve water efficiency, reducing leakages and improving services to help contribute to the sustainable management of water resources in areas with data centers.

Addressing the Planning Gap

The trajectory of data center development does not have to be one of compounding resource strain and reactive governance — but to avoid that, deliberate choices must be made. Choices that run against the grain of emerging and established trends. And they have to be made fast.

Today, the most likely scenario is one shaped by competing interests where risks are shared, but the benefits aren’t. Where the jobs created and taxes paid arguments win in the short term and where fragmented governance across national, regional and municipal authorities leaves critical decisions uncoordinated.

However, data centers can contribute to their local economies if they commit and invest in those communities. Otherwise, fragile grids and constrained water systems will continue to host large-scale ambitions, while each approved development raises the baseline pressure on the next, compounding a problem that isn’t even fully understood yet.

A best-case scenario demands coordinated reform: policymakers must incentivize water efficiency and infrastructure investment; investors need to price in long-term resource risk; and the industry must prioritize investment in water resilience alongside energy and infrastructure. Community benefit agreements and policy incentives should be seen as frameworks for sustainable growth because if taps run dry, so does business.

Policymakers, investors, industry leaders and utility providers must see — and address — water resilience as an issue critical to business resilience.

This article is published as part of a project between the Australian Water Partnership (AWP) and the Alliance for Global Water Adaptation (AGWA) which seeks to equip cities and regions in the Indo-Pacific with the policy frameworks, knowledge, and tools they need to not just survive an AI boom but thrive in it. Read more >